Announcements

Jan 12, 2021

For BPI Auto / Housing Loan clients whose incomes had been affected by the pandemic, and are in need of additional relief on their loan payments, here are 4 sample payment options that may help you manage your existing loan obligations:

Original Loan Details (Sample) | ||||

|---|---|---|---|---|

Due Date | Monthly Due | Principal | Interest | Outstanding Balance |

November 10, 2020 | - | - | - | Php 419,000 |

December 10, 2020 | Php 37,000 | Php 34,000 | Php 3,000 | Php 385,000 |

January 10, 2021 | Php 37,000 | Php 34,000 | Php 3,000 | Php 351,000 |

February 10, 2021 | Php 37,000 | Php 34,000 | Php 3,000 | Php 317,000 |

March 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 282,000 |

April 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 247,000 |

May 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 212,000 |

June 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 177,000 |

July 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 142,000 |

August 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 107,000 |

September 10, 2021 | Php 37,000 | Php 35,000 | Php 2,000 | Php 72,000 |

October 10, 2021 | Php 37,000 | Php 36,000 | Php 1,000 | Php 36,000 |

November 10, 2021 | Php 37,000 | Php 36,000 | Php 1,000 | Php 0 |

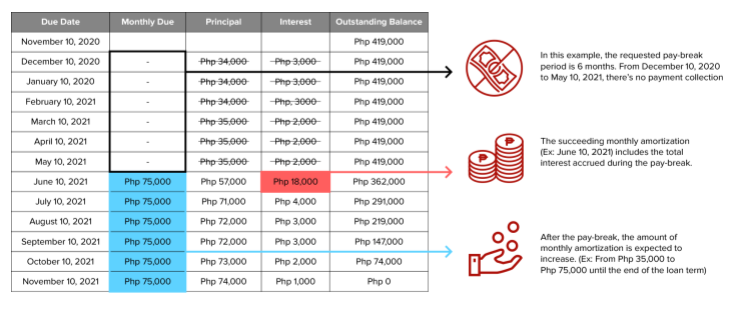

1. Pay-Break (Grace Period)

- A loan pay-break, or more commonly known as a grace period, is a temporary suspension of payment collection for specific amortization due dates.

- Your original loan term (maturity date) will remain the same but your monthly amortization after the pay-break will increase to allow you to catch-up with the missed payments during the pay-break.

- The principal loan balance shall continue to earn accrued interest, and your first monthly amortization after the pay-break will be first applied towards the accrued interest which had accumulated over the grace period.

- During a grace period, no late penalty fees or interest-on-interest will be charged, while the unpaid loan principal shall continue to accrue interest.

Example:

In this example, the requested pay-break period is 6 months. From December 10, 2020 to May 10, 2021, there’s no payment collection.

Php 18,000 Interest = The succeeding monthly amortization (Ex: June 10, 2021) includes the total interest accrued during the pay-break.

Php 75,000 Monthly Due = After the pay-break, the amount of monthly amortization is expected to increase (Ex: From Php 35,000 to Php 75,000 until the end of the loan term).

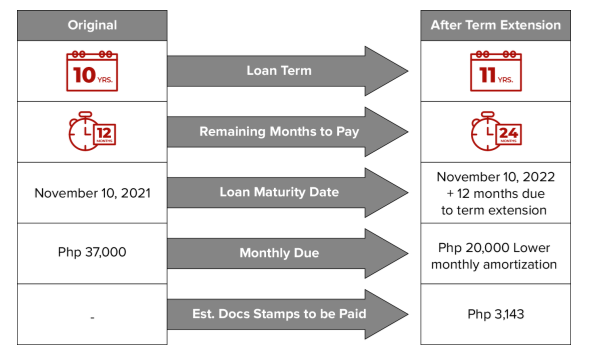

2. Term Extension

- Your original loan term (maturity date) will be extended and moved to a later date. As a result, the amount of your monthly loan amortization will be re-computed and re-distributed using the new loan term.

- Under a term extension, you will have lower monthly installment amounts versus your original monthly amortization due. Payment collection every month shall proceed, without breaks or grace period.

- Due to the amendments made, payment for Documentary Stamp Tax shall be collected from the client.

Example:

3. Pay-Break + Term Extension

- Under this option, both pay-break and term extension shall be applied on your loan. As a result, payment collection on specific due date/s shall be temporarily suspended.

- Once the pay-break ends, your original loan term shall be moved to a later date, and your re-computed monthly installment shall be the basis for payment collection.

- Due to the amendments made, payment for Documentary Stamp Tax shall be collected from the client.

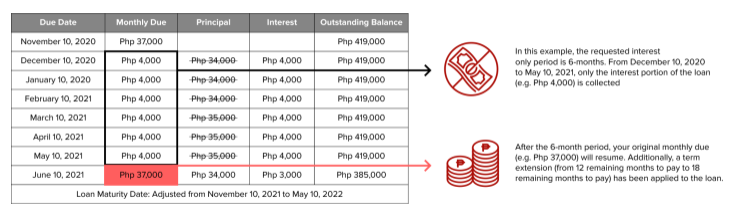

4. Short-term Interest-Payments Only

- Another option that may help augment your cash flow is to allot payments on the loan’s interest portion only, within a specific and finite period.

- After the interest-payment-only period, you have an option to: 1. keep your original loan term (where your monthly amortization will increase to allow you to catch-up with the missed principal payments during the interest-payment only period) or 2. extend your term (where your monthly installment will be re-computed, subject to Documentary Stamp Tax).

Example:

Php 4,000 Monthly Due = In this example, the requested interest only period is 6-months. From December 10, 2020 to May 10, 2021, only the interest portion of the loan (e.g. Php 4,000) is collected.

Php 37,000 Monthly Due = After the 6-month period, your original monthly due (e.g. Php 37,000) will resume. Additionally, a term extension (from 12 remaining months to pay to 18 remaining months to pay) has been applied to the loan.

Terms and Conditions

1. All requests are subject to the evaluation and approval of the Bank.

2. Evaluation shall only begin upon submission of complete initial requirements, which include valid IDs, income documents based on source of income, and Special Power of Attorney (if submitting a request on behalf of the borrower).

3. During the evaluation, the Bank may ask for additional documents / requirements apart from what borrowers have previously submitted.

4. Borrowers are strongly advised to continue paying the original monthly dues while the request is being processed to avoid incurring additional charges and penalties.

5. Upon approval, borrowers shall sign a Conforme Letter and/or other pertinent documents in any BPI branch or using an electronic online signing platform deemed appropriate by and acceptable to the Bank.

6. Payment of appraisal fee, notarial fee and Documentary Stamp Taxes and other Bank charges shall be required as applicable.

How to request for Loan Relief

1. Go to our Online Loan Relief Inquiry Form and provide all the requested information.

2. In the Loan Relief Scheme field, please choose your preferred option: Pay-break, Term Extension, Pay-break + Term Extension, or Short-term Interest-Payments-Only

3. After clicking "Submit", you will immediately receive an auto-generated e-mail from bpiloans@bpi.com.ph. This contains your agreement to the Terms & Conditions of the Loan Relief Scheme.

4. All submitted requests will be reviewed by our credit officers.

5. We will contact you to confirm your preferred date and time to receive our call.